When you’re in the early days of your working life, retirement may seem distant, and your super unimportant. However, by planning and acting early, you can make the most of compounding returns to grow your super balance over the long-term, giving you peace of mind that you’ll have financial freedom when you decide to stop working.

Start simple and get the basics sorted

The first and arguably one of the most important steps in your super journey is getting the basics sorted.

Know your Super Guarantee rights

Super Guarantee (SG) contributions will be paid consistently throughout your working life, likely forming the foundation of your super balance – so it’s important you understand the rules relating to them.

While there are a number of rules you should be aware of, most importantly your employer is typically required to make SG contributions on your behalf to your super account within 7 business days of your payday. SG contributions are normally calculated as a percentage of your Qualifying Earnings. From 1 July 2025, the percentage is 12%.

Visit our dedicated Super Guarantee (SG) webpage to learn more about your employer’s responsibilities and what you can do if you think your employer has made a mistake.

Nominate your choice of super fund

As it's your super, it's your choice which super fund your employer pays it to.

Visit our dedicated Choice information webpage to learn more, including how to nominate Mercer Super as your choice of super fund.

Review your investment option choice

Once you’ve decided on a super fund, you should consider what type of investment option(s) you’d like to be invested in.

Younger people typically have a long investment time frame of 30 years or more, meaning your investments have time to recover from any short-term losses, so you might target long-term growth over security.

But your personal circumstances are unique, so it may be worth seeking advice. Most Mercer Super members have access to e-Advice, a self-service tool, designed to provide the advice you need to make investment decisions for your personal circumstances.

Sacrifice a little salary today for a big boost to your super tomorrow

Salary sacrificing lets you contribute to your super, while also reducing the amount of income tax you pay.

By asking your employer to contribute even a small additional amount of your take-home pay to your super account each time you're paid money that you otherwise would’ve paid as tax is deposited into your super account.

If done over decades, or even just several years, salary sacrificing can provide a significant boost to your super balance by the time you reach retirement age.

Visit our dedicated salary sacrifice webpage to learn more about the benefits and other considerations.

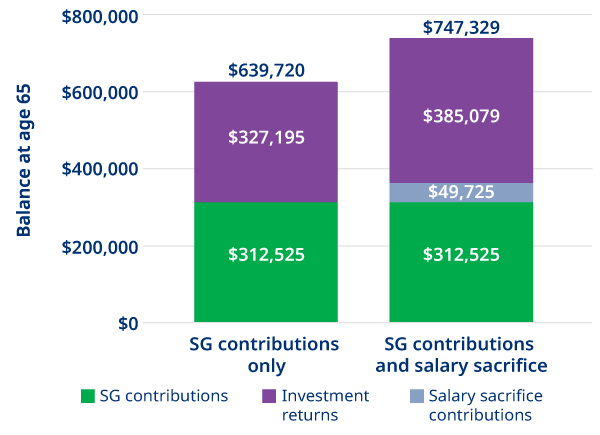

Example: salary sacrificing $50 a fortnight1

Let the government lend a hand

The super co-contribution is an Australian Government initiative, helping low and middle-income earners add money to their super.

Under the scheme, the Australian Government will automatically contribute up to $500 to your super account, if you make a personal contribution to your super and meet their eligibility criteria.

Don’t hope for the best, plan for it with financial advice

As a Mercer Super member you can have access to financial advice about your super at no additional cost. Talk to us now to learn more about your options.

Read next:

Grow your super

From your first job to retirement, take steps to boost your super and secure your financial freedom.

Ages 30-58: Building momentum

During this stage, many people are well into their careers, often earning more than when they were younger.

Ages 59 and beyond: Balancing withdrawals and growth

As retirement draws closer, people often look to downsize their home or work less, but not retire completely.

1 Assumptions: Superannuation Guarantee (SG) contributions commenced at age 18 in 2026 and ceased at age 65. Salary sacrifice arrangement is $50 per fortnight, commencing at age 20 and ceasing at age 65. All future figures have been discounted for inflation. Salary based on median all-persons income from abs.com.au, last released in 2022/23. SG is 12%. Growth oriented super based returns of 3.75% p.a. after inflation. Difference in returns (which may be positive or negative) and fees will alter the outcome. Future government decisions relating to contribution caps have been assumed to remain high enough to accommodate all contributions. The example shown may not apply to your own situation, so we recommend you consider your options carefully and seek financial advice if you’re unsure if making additional contributions is right for you. Past performance should not be relied upon as an indicator of future performance.

Please note that any information on tax or references to legislation in this material is based on our interpretation of current laws which are subject to change. We recommend you obtain your own tax or other professional advice when considering the application and impact of tax laws or other laws that may affect you. No warranty as to the accuracy or completeness of this information is given and no responsibility is accepted by Mercer or any of its related entities for any loss or damage arising from reliance on the information.

Issued by Mercer Superannuation (Australia) Limited (MSAL) ABN 79 004 717 533, Australian Financial Services Licence #235906, the trustee of Mercer Super Trust ABN 19 905 422 981 (‘Mercer Super’).

Any advice provided is of a general nature and does not take into account your objectives, financial situation or needs. Before acting on any advice we recommend you obtain your own financial advice and consider the Product Disclosure Statement and Financial Services Guide available at mercersuper.com.au. The product’s Target Market Determination setting out the class of people for whom the product may be suitable can be found at mercersuper.com.au/tmd.

‘MERCER’ and 'Mercer SmartPath®' are Australian registered trademarks of Mercer (Australia) Pty Ltd ABN 32 005 315 917.

Past performance is not a reliable indicator of future performance. The value of an investment in the Mercer Super Trust may rise and fall from time to time. The investment performance, earnings or return of capital invested are not guaranteed.