Regardless of your age, it's never too early or too late to start thinking about retirement and working towards maximising your super, for an improved tomorrow. From your first job to retirement, there's steps you can consider taking to help improve your financial future.

Compounding returns – the secret ingredient to your super’s success

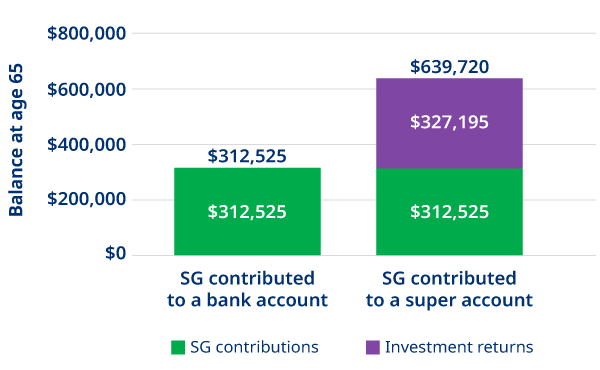

One of the largest and often overlooked contributors to your super balance will be the ability for your returns to compound over time.

What this means is that the returns earned on your contributions don’t just sit idle, those returns go on to earn more returns, which go on to earn even more returns, forming a cycle of growth that for the majority of people leads to an enormous increase in their super balance over the long haul.

By consistently adding money to your super coupled with the power of compounding investment returns, your balance has the potential to snowball over the years.

Although the magic of compounding returns is beneficial to everyone, it can be particularly advantageous if capitalised on early, as the earlier you start, the more time this process has to work.

Example - SG contributed to an everyday transaction bank account vs. a super account1

Super-boosting strategies for all ages

While some super-boosting strategies may be better suited to an individual based on their age, there are others which are beneficial regardless of age.

Consider combining your super and avoid unnecessary fees

Having more than one super account could mean you’re paying multiple fees, Although these fees may not seem like much now, over several years, or even decades, it can have a significant impact on your balance by the time you reach retirement.

Visit our dedicated consolidation webpage to learn more about the benefits of consolidating your super, what you should consider and how to do it.2

Ensure your investment strategy aligns with your goals

As your life and financial goals change over time, your super investment strategies should too.

Visit our dedicated investment webpage to learn more about our history of positive long-term performance.†

Check your super fund is working as hard as you are

Not all super funds are made equal. With each super fund performing differently, how your super fund performs over the long-term can make a significant difference to your final balance – especially when combined with low fees.

Visit our dedicated performance webpage to learn more about our history of positive long-term performance.† Or visit our dedicated fees webpage to learn more about fees and costs you pay.

Age-based super-boosting strategies

While the above strategies can be beneficial to people of all ages, there are some super-boosting strategies better suited to specific age groups.

Younger than 30: Laying the foundation

For those in the early days of their working life you have one of the most powerful super building strategies available to you. You have time.

By planning and taking action early, you can make the most of compounding returns, significantly increasing your super balance over the long-term.

Ages 30-58: Building momentum

During this stage, many people are well into their careers, often earning more than when they were younger.

This may mean you can turn up the heat on your super contributions, or, if you have one, team up with your spouse to get the most out of your super.

Ages 59 and beyond: Balancing withdrawals and growth

As retirement draws closer, people often look to downsize their home or work less, but not retire completely.

With this in mind there are still opportunities for you to continue getting the most out of your super.

Considerations before making contributions

Contribution caps

While adding extra to your super can be a good strategy, there are rules around how much you can add without tax implications – these are known as ‘contribution caps’.

Visit our dedicated contribution caps webpage to learn more about the caps, including how much you can contribute, which contributions count towards which cap, as well as implications for exceeding either of the caps.

Seek financial advice

Everyone’s situation and objectives are different, which means there’s no ‘one-size fits all’ strategy when it comes to financial advice. As a Mercer Super member you have access to a range of financial advice and support tools at no additional cost.

Visit our dedicated financial advice webpage to learn more about the different forms of financial advice available to you and how to access them.

Past performance is not a reliable indicator of future performance. The value of an investment in the Mercer Super Trust may rise and fall from time to time. The investment performance, earnings or return of capital invested are not guaranteed.

† Mercer Super’s default investment option Mercer SmartPath has delivered 9.0% p.a. for the 10-year period to 30 June 2026 for one of our largest groups of members. Based on Mercer SmartPath membership data as at 31 March 2026 and for members invested for the full period. Mercer Super Trust’s analysis of Mercer SmartPath (born 1984-88), after investment fees and taxes.

1. Assumptions: Superannuation Guarantee (SG) contributions commenced at age 18 in 2026 and ceased at age 65. All future figures have been discounted for inflation. Salary is based on the median all-persons income from abs.com.au, last released in 2022/23. SG is 12%. While SG contributions cannot legally be made directly to a bank account, this example uses the scenario of SG held in an everyday bank account purely for illustrative purposes. This approach aims to highlight the impact of compounding investment returns more simply over an extended period. Bank interest is assumed to be paid at the inflation rate, resulting in no real earnings. Growth-oriented superannuation returns are assumed to be 3.75% p.a. after inflation. Differences in returns (which may be positive or negative) and fees will alter the outcome. Future government decisions relating to contribution caps have been assumed to remain high enough to accommodate all contributions. The example shown may not apply to your own situation. We recommend you consider your options carefully and seek financial advice if you’re unsure whether making additional contributions is right for you. Past performance should not be relied upon as an indicator of future performance.

2. Combining your super can be a significant financial decision. If you decide to combine all or part of your other super account(s), carefully consider how this may have an impact on your existing insurance, contribution and tax arrangements, fees or charges, or any other benefits you may lose. If you intend to claim a tax deduction on your personal contributions, you will need to provide your existing fund with a notice of intent to claim and receive confirmation it's been processed before combining your super. We recommend you seek financial advice before deciding whether to combine your super accounts.

Any information on tax in this document is based on our interpretation of current tax laws which are subject to change. We recommend you obtain your own tax advice when considering the application and impact of tax laws that may affect you. No warranty as to the accuracy or completeness of this information is given and no responsibility is accepted by Mercer or any of its related entities for any loss or damage arising from reliance on the information.

Issued by Mercer Superannuation (Australia) Limited (MSAL) ABN 79 004 717 533, Australian Financial Services Licence 235906, the trustee of Mercer MyChoice which is part of the Mercer Super Trust ABN 19 905 422 981 (‘Mercer Super’).

Any advice provided is of a general nature and does not take into account your objectives, financial situation or needs. Before acting on any advice we recommend you obtain your own financial advice and consider the Product Disclosure Statement and Financial Services Guide available by logging into your account.

‘MERCER’ is an Australian registered trademark of Mercer (Australia) Pty Ltd ABN 32 005 315 917.

Past performance is not a reliable indicator of future performance. The value of an investment in the Mercer Super Trust may rise and fall from time to time. The investment performance, earnings or return of capital invested are not guaranteed.