As you enter this next stage of life, you may be looking to looking to retire, or just work a little less. That doesn't mean your super can't still keep working for you though – this stage of life brings with it several strategies that can help give your super a leg up.

Downsize your home and upsize your super

As people get closer to retirement age they may choose to downsize their home as their life circumstances change.

This presents a significant opportunity if you’re aged 55 or over, because you can make a one-off super contribution of up to $300,000, using proceeds from the sale of your primary residence.

If you have a spouse, they may also have the option to contribute up to $300,000 to their super – bringing the total contribution amount up to $600,000 per couple.

Although this contribution will undoubtedly bolster your super balance, it’s also uniquely flexible in that:

- There is no age limit on this contribution

- It doesn’t matter if you’re working full-time, part-time or retired

- it doesn’t count towards either of the contribution caps – meaning there isn’t a risk of the contribution being taxed.

You can learn more about the eligibility criteria, as well as how to make a downsizer contribution on the ATO’s website.

Example: $300,000 downsizer contribution1

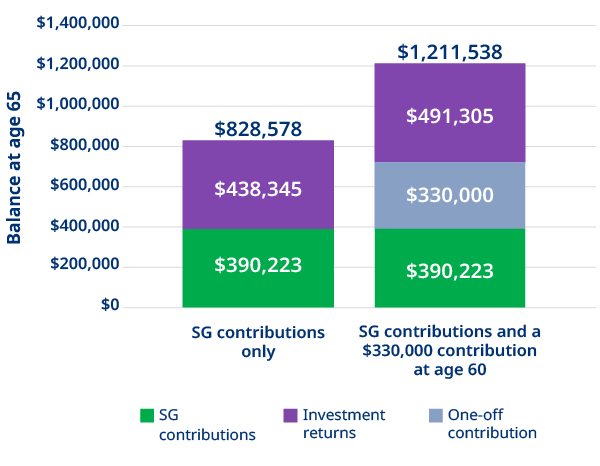

Make up to 3 years’ worth of personal contributions

While the annual cap on personal contributions is $130,000, the bring-forward rule allows you to contribute up to three years’ worth of contributions at once – totalling $390,000.

This is particularly useful in situations where individuals have come into a large sum of money such as an inheritance and are looking to significantly boost their super quickly without tax implications.

You can learn more about bring-forward rule, including eligibility criteria on our dedicated contribution caps page.

Example: $390,000 one-off contribution2

Work less and let your super share the load

If you're nearing retirement age and want to work a bit less, a transition to retirement strategy may be useful. You can access some of your super while still working part-time, helping you maintain your lifestyle while potentially reducing your taxable income.

Learn more about using your super to transition to retirement, including benefits, eligibility criteria, how to do it and other considerations on our retirement hub.

Don’t hope for the best, plan for it with financial advice

As a Mercer Super member you can have access to financial advice about your super at no additional cost. Talk to us now to learn more about your options.

Read next:

Grow your super

From your first job to retirement, take steps to boost your super and secure your financial freedom.

Younger than 30: Laying the foundation

As a younger person you have one of the most powerful super building strategies available to you. You have time.

Ages 30-58: Building momentum

During this stage, many people are well into their careers, often earning more than when they were younger.

1. Assumptions: Superannuation Guarantee (SG) contributions commenced at age 18 in 2026 and ceased at age 65, as well as a one-off downsizer contribution of $300,000 at age 59. All future figures have been discounted for inflation. Salary based on median all-persons income from abs.com.au, last released in 2022/23. SG is 12%. Growth oriented super based returns of 3.75% p.a. after inflation. Difference in returns (which may be positive or negative) and fees will alter the outcome. Future government decisions relating to contribution caps have been assumed to remain high enough to accommodate all contributions. The example shown may not apply to your own situation, so we recommend you consider your options carefully and seek financial advice if you’re unsure if making additional contributions is right for you. Past performance should not be relied upon as an indicator of future performance.

2. Assumptions: Superannuation Guarantee (SG) contributions commenced at age 18 in 2026 and ceased at age 65, as well as a one-off after-tax contribution of $390,000 at age 60. All future figures have been discounted for inflation. Salary based on median all-persons income from abs.com.au, last released in 2022/23. SG is 12%. Growth oriented super based returns of 3.75% p.a. after inflation. Difference in returns (which may be positive or negative) and fees will alter the outcome. Future government decisions relating to contribution caps have been assumed to remain high enough to accommodate all contributions. The example shown may not apply to your own situation, so we recommend you consider your options carefully and seek financial advice if you’re unsure if making additional contributions is right for you. Past performance should not be relied upon as an indicator of future performance.

Please note that any information on tax or references to legislation in this material is based on our interpretation of current laws which are subject to change. We recommend you obtain your own tax or other professional advice when considering the application and impact of tax laws or other laws that may affect you. No warranty as to the accuracy or completeness of this information is given and no responsibility is accepted by Mercer or any of its related entities for any loss or damage arising from reliance on the information.

Issued by Mercer Superannuation (Australia) Limited (MSAL) ABN 79 004 717 533, Australian Financial Services Licence #235906, the trustee of Mercer Super Trust ABN 19 905 422 981 (‘Mercer Super’).

Any advice provided is of a general nature and does not take into account your objectives, financial situation or needs. Before acting on any advice we recommend you obtain your own financial advice and consider the Product Disclosure Statement and Financial Services Guide available at mercersuper.com.au. The product’s Target Market Determination setting out the class of people for whom the product may be suitable can be found at mercersuper.com.au/tmd.

‘MERCER’ and 'Mercer SmartPath®' are Australian registered trademarks of Mercer (Australia) Pty Ltd ABN 32 005 315 917.

Past performance is not a reliable indicator of future performance. The value of an investment in the Mercer Super Trust may rise and fall from time to time. The investment performance, earnings or return of capital invested are not guaranteed.